Kansas is a powerhouse in American agriculture, with over 45 million acres of farmland across the state.

For independent agents quoting Kansas farm insurance, understanding the unique risks and coverage needs of operations in this region is essential.

Here are a few important underwriting factors for agents to consider.

Weather Risks Are Wide-Ranging

Farms across Kansas face year-round weather threats that directly impact Kansas farm insurance quoting and coverage needs.

Some key concerns:

- Hail: Frequent storms can cause significant damage to equipment, roofing, vehicles, and structures.

- Tornadoes: High-value equipment and structures like barns and center pivots are particularly at risk.

- Drought and flooding: Depending on the region, farmers may experience both in a single season, impacting operational continuity and property damage.

Because these risks are common and often severe, underwriters look closely at the presence of high-value equipment, claims history, and how the property is maintained or reinforced against storms.

For agents, it’s critical to ensure all structures and equipment are accurately scheduled with appropriate coverage types, particularly those susceptible to weather damage.

Why Irrigation Systems Matter in Kansas Farm Insurance Policies

Irrigation is central to many Kansas farms, and center pivot systems often represent some of the most valuable and vulnerable assets on the property.

These systems are exposed to wind, hail, tornadoes, lightning, mechanical failure, and collision.

A few things to consider during quoting:

- Coverage structure: Is the irrigation equipment covered under a separate irrigation policy or under a broader farm and ranch policy?

- Valuation type: Does the policy reimburse replacement cost or actual cash value?

- Attachments: Ensure coverage for connected components like pumps, motors, electrical panels, towers, and control systems.

- Underwriting criteria: The age of the unit, prior claims, and system maintenance are all factors that can influence rating and eligibility.

Standard farmowners’ policies often lack sufficient coverage for center pivots. If you’re working with Kansas farm insurance clients who rely heavily on irrigation systems, be sure to explore standalone irrigation options, including carrier partners like Chubb and Aegis Agribusiness.

Insuring Kansas Specialty Crop Operations

While irrigation remains a key tool, many Kansas farms are also adapting by planting specialty crops like sorghum, sunflowers, and pulses that can thrive with less water. These crops can increase farm resilience and open up new market opportunities, but they also introduce new exposures.

Liability

Direct sales, agritourism, and custom processing increase liability risks to farming operations.

- Tip: Discuss new activities with your client, then confirm exclusions and coverage needs with the carrier; endorsements or separate policies may be required.

- Note: Stroud National does not typically cover agritourism or custom processing. Direct sales may be acceptable on a case-by-case basis, provided farming remains the primary source of income.

Business interruption

Multi-stage storage and processing can lead to new sources of income loss in the face of delays and equipment breakdowns.

- Tip: Confirm whether business interruption and extra expense coverage applies across these stages.

Off-farm risks

Sales contracts or third-party processing may fall outside standard farm policy protections.

- Tip: Ensure the policies in place reflect the full scope of your client’s current activities.

- Note: Stroud typically covers on-farm risks; off-farm and contract exposures need separate coverage.

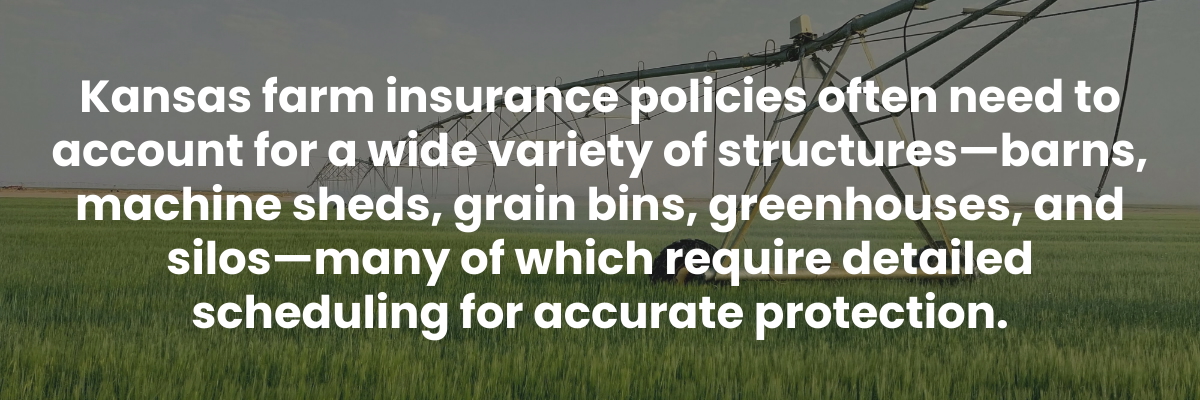

Equipment, Outbuildings, and Property Must Be Scheduled Accurately

For a stronger submission:

- List structure type, usage, size, and construction details.

- Clearly identify personal vs. farm use for dual-purpose buildings (e.g., barndominiums).

- Confirm that insured values reflect current rebuild costs and local material availability.

- Note any equipment shared with or leased to others, especially if liability is a concern.

Quoting Kansas Farm Insurance: What to Include in Every Submission

To help underwriters place Kansas farm insurance quickly and accurately, a detailed and thoughtful submission is key.

Include:

- All property and building details (age, size, usage, construction type, value)

- Equipment lists with current valuations

- Irrigation systems and component information (for standalone options, see carrier details)

- Details about crops and livestock on the property

- Claims history and mitigation practices

Quoting Kansas farm insurance? Whether you need admitted or non-admitted coverage, we’ve got you covered.

Start the quoting process by completing our Farm and Ranch Online Quote Request Form and reach out to our Farm and Ranch underwriters with questions.

For quoting guidance for standalone irrigation, please reach out to our irrigation underwriting team.

We’re happy to help!